ISM Manufacturing PMI Beats Expectations, Gold Prices Slip

The ISM manufacturing purchasing managers’ index (PMI), which measures economic activity in the national manufacturing sector, rose from 43.1 to 52.6 vs. 49.5 expected in June. A reading over 50 indicates positive growth, and June marks the first expansion in the industry since the COVID-19 pandemic struck in April 2020, ending a 131-month string of consecutive growth.

Key Takeaways

- The ISM manufacturing index came in at 52.6 vs. 43.1 the month before and 49.5 expected.

- While the headline figure indicates expansion, many key indexes are still in contraction territory, and most of the growth was in prices.

- New orders hit a 14- month high in the ISM figures, while the Markit manufacturing PMI is still in contraction.

The manufacturing PMI is now in expansion territory. New orders rose 24.6 points from 31.8 in May to 56.4 in June. Production rose 24.1 points to 57.3 points. The backlog of orders rose 7.1 points to 45.3, and employment rose 10 points to 42.1. Meanwhile, supplier deliveries fell 11.1 points to 56.9.

The inventories index rose 0.1 points to 50.5, prices rose 10.5 points to 51.3, new export orders rose 8.1 points to 39.5, and imports rose 7.5 points to 41.3. Overall, supplier deliveries are slowing at a slower rate. Employment is contracting. Customer inventories are too low, prices are increasing, and exports and imports are contracting.

US recovers faster than expected.

ISM Manufacturing, new orders arise to 14-month high, back in expansion.

However, Markit manufacturing PMI remains in contraction despite the massive bounce.

ADP jobs came at 2.369m. Slightly below expectations but huge revision in May. pic.twitter.com/wRo2AQpZWB

— Daniel Lacalle July 1, 2020

Out of 18 industries total, 13 reported growth in June, led by Textile mills, wood products, furniture and related products, printing and related support activities, leather and allied products, as well as food, beverage and tobacco products. The food and beverage industry has been seriously impacted by the COVID-19 lockdown procedures in place to varying degrees throughout the US in recent months. Meanwhile, four industries reported contraction. Those were transportation equipment, primary metals, fabricated metal products, and machinery.

Expert Outlook

"As predicted, the growth cycle has returned after three straight months of COVID-19 disruptions. Demand, consumption and inputs are reaching parity and are positioned for a demand-driven expansion cycle as we enter the second half of the year,” said Timothy Fiore, Chair of the ISM's Manufacturing Business Survey Committee.

“Among the six biggest industry sectors, Food, Beverage & Tobacco Products remains the best performing industry sector, and Computer & Electronic Products, and Chemical Products returned to respectable growth. Transportation Equipment and Fabricated Metal Products continue to contract, but at much softer levels," added Fiore.

A respondent from the transportation industry wrote that they were "Gradually ramping production back in our plants. Most of our supply base continued to operate during COVID-19, so we are not seeing a significant supply risk. Will be monitoring supply chain financial health closely."

Market Reaction

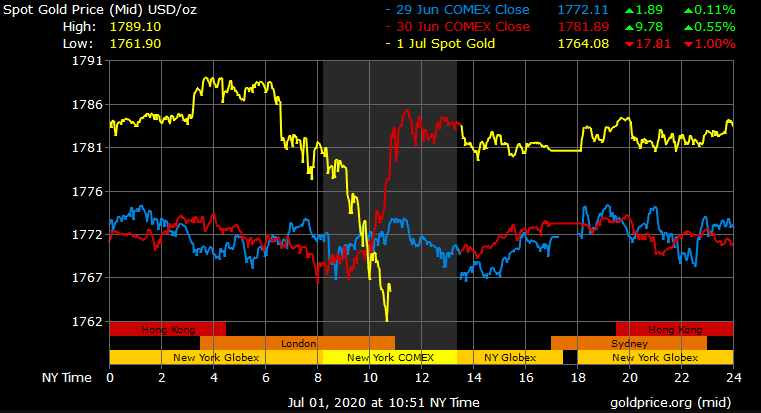

Gold prices have faced selling pressure following the release of the manufacturing report. Spot gold last traded at $1,764.08/oz, down -1.0% with a high of $1,789.10/oz and a low of $1,761.90/oz. With the manufacturing industry re-entering an overall growth, risk-on appetite has increased in the market, leading some traders to abandon gold as a safe haven in the short term. Gold sunk to daily lows following the report, after hitting the highest price point in over eight years overnight.

Gold Price Chart

More articles from Conor Maloney